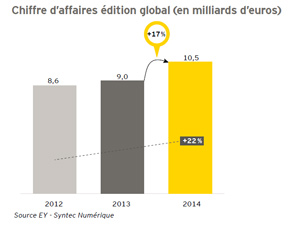

More than 10 billion turnover in 2014 (+ 17% compared to 2013), steady growth of the workforce in France and abroad, operations, financing and acquisitions on the increase, the continued investment in innovation …

The software publishing industry confirms more than ever its locomotive role in the economy, particularly in terms of growth and job creation. This is what shows the 5 th edition of the Top250 directed by EY firm and Syntec Numérique (To download Panorama Top 250 French software publishers and creators).

If national champions top 10 publishing have contributed to this result, with an increase of 22% of their turnover, editors “out top 10″ still show 10% growth, demonstrating the general dynamism of the French software publishing. SMEs of less than 10 million euros even recorded an average increase of 25% of their business, so they do not count as startups in their ranks.

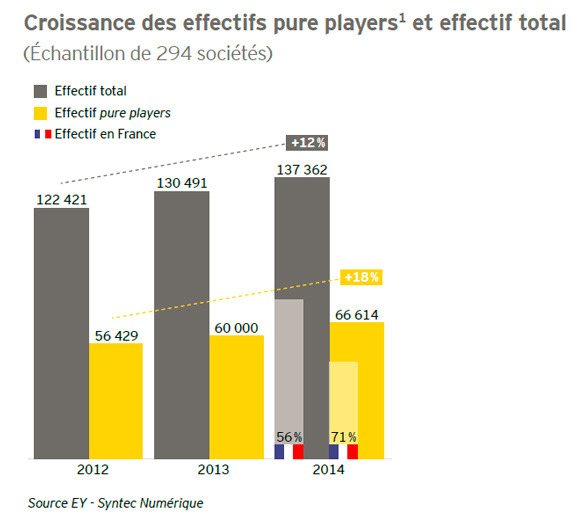

This exceptional growth benefits the whole of French society, including on the employment front. In two years, French software companies have created more than 15,000 jobs.

This dynamism also covers companies in other sectors, accompanied in their digital transformation, gaining competitiveness.

The SaaS channel, which remains the No. 1 priority technology publishers, continued to grow, representing 22% of their activity, against 17% the previous year. A movement that should not be hindered “tax inventiveness” excessive, which could weigh on the Cloud and the extension of the scope of the private copying levy, which would burden the competitiveness of SaaS in France.

Other technological priorities of French publishers are mobility, security and of course the Big data! Publishers have a major role to play in helping their customers to go further in the value of their data.

Confident in the future, 82% of software companies plan to hire in the coming month

To accelerate growth, SMEs maintain their R & amp effort. D around 20% of sales, large companies to 11%. R & amp;. D whose numbers remain three quarters in France, including the use of CIR regarding 77% of publishers

Finally, Editors also use internationally for growth, even if the exposure of large companies – two-thirds of sales – still much higher than that of SMEs. For the latter, the strong momentum in external growth – an editor on two plans an operation is an option to confront markets increasingly globalized

edition. Top250 in 4 key points:

- Creating and editing software: a sector under the sign of dynamism

The dynamism of the sector affects all industry players with nevertheless a significant contribution of the top ten publishers in our sample (22%). Out front runners, the growth rate is 10%.

With cumulative growth rate over 2 years s’ amounting to 22 and 25% respectively, sectoral and horizontal publishers confirm the strong dynamism of the sector. The “Personal and games” segment reported a growth rate of 15%, a performance essentially attributable to two heavyweights of the French game. Ubisoft and Gameloft

With cumulative growth rate over 2 years s’ amounting to 22 and 25% respectively, sectoral and horizontal publishers confirm the strong dynamism of the sector. The “Personal and games” segment reported a growth rate of 15%, a performance essentially attributable to two heavyweights of the French game. Ubisoft and Gameloft

The editors remain highly concentrated with 68% of sales ‘turnover by 7% of publishers. All publishers contribute to the strong growth of the sector irrespective of their size. Publishers generating less than € 10 million turnover registered a growth rate of 25% over 2 years.

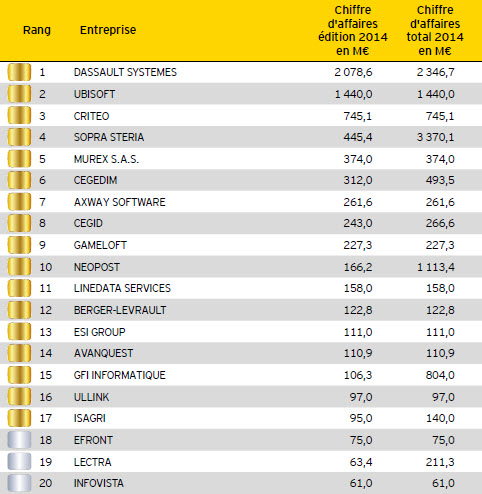

The 2015 edition of the Top250 shows the positive correlation between business growth and the degree of internationalization of the company: companies under € 10 million overwhelmingly operate in the French market, while very large organizations (over € 100 million) such as DS, Ubisoft or Criteo realized 64% of their turnover abroad in 2014, against 50% in 2014

- Talents. recruit, retain

Nearly 15,000 jobs in 2 years: job creations were up 12% over the period 2012-2014. Moreover, the share of employees based in France (56%) is stable or even increased slightly since 2012

- Innovation: an ever faster rate

The share of revenues paid to the R & amp; D remains very high ( 13%), which is particularly noticeable in small organizations (20%). The deep roots of R & amp; D on French soil reflects, among other things, the effectiveness of innovation support schemes set up by the State

77% of publishers. French software will have used the research tax credit in 2014 to fund innovation. Tax audits related CIR seem to initiate a slight decline: 22% of surveyed publishers experienced a tax audit for the CIR in 2014 (against 34% in 2013)

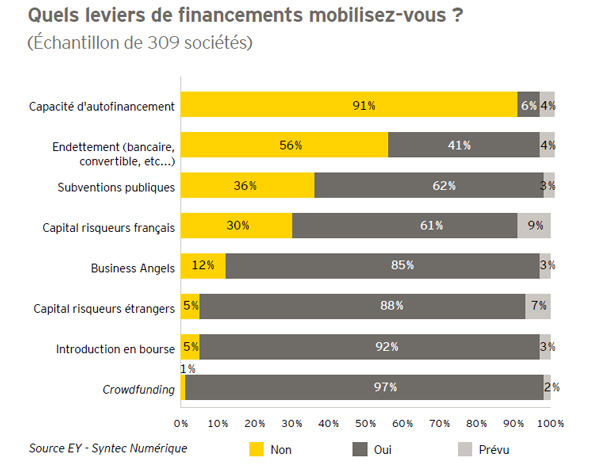

The use of French venture capital and abroad (35%) and Foundations (12%), are on the increase and demonstrate the interest of investors in this sector. The use of BPI France is still very common in the Vendor financing strategy. In combination with other means of financing, such as venture capital funds, the institution allows start-ups and SMEs to overcome the effects of thresholds and change scale in an environment where they find it difficult to grow.

- Growth opportunities: SaaS, mobility, security and Big data

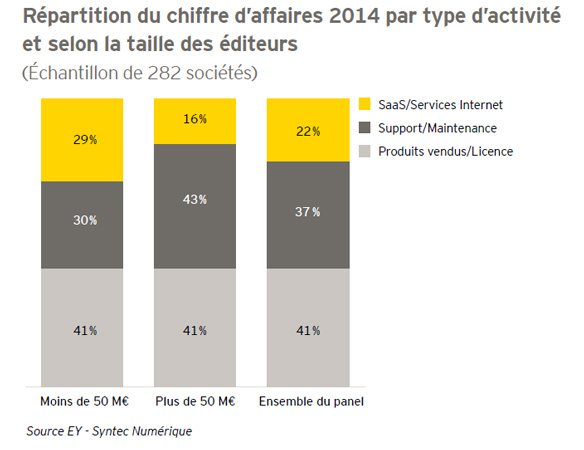

SaaS is everything as a strategic change, technological, and commercial. Investment in the Cloud and SaaS by French companies responding to global agility needs dictated by the digital economy and the need to develop business models around the uses and users. The share of SaaS (Software as a Service) and Internet services in the activity of publishers continues to grow, with 22% of sales in 2014, against 17% in 2013.

The proportion of sales generated in Saas is also greater among actors under € 50 million in revenue held account technical and financial constraints posed by the switch to this model.

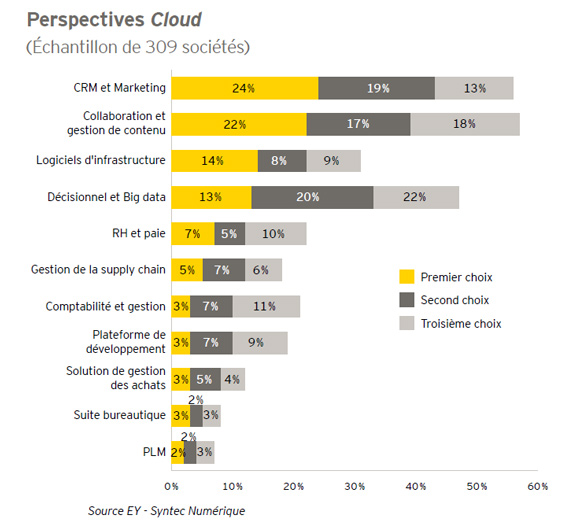

CRM and marketing activities are perceived as the main source of opportunity with cloud collaboration and content management.

The infrastructure software and decision and Big data are also considered important growth levers: they account for 14% and 13% of the vote

No comments:

Post a Comment